Posted by Edward Yoder in Not-for-Profit, Tax: Exempt Organizations.

Unrelated Business Taxable Income (UBTI) reporting for exempt organizations can be challenging, particularly if the exempt organization has invested in one or more partnerships. The instructions to Form 1065 partnership returns direct preparers to report any information a partner that is a tax-exempt organization may need to figure its share of unrelated business taxable income under Internal Revenue Code (IRC) Section 512(a)(1). Partners are required to notify the partnership of their tax-exempt status.

IRC Section 512(a)(1) – UBTI means the gross income derived by any organization from any unrelated trade or business regularly carried on by it, less the deductions directly connected with the carrying on of such trade or business. To be UBTI, the income must meet all three components:

- Income from a trade or business that is,

- Regularly carried on, and

- Not substantially related to an exempt purpose

Even if there is an exception to UBTI, such as the exception for investment income or rental real estate, the income may still be subject to UBTI if it is debt-financed. Debt-Financed Property Section 514(b)(1) – Debt-financed property means any property which is held to produce income and with respect to which there is an acquisition indebtedness at any time during the tax year or preceding 12-month period, if the property was disposed of during the tax year.

This rule can be especially important for exempt organizations investing in partnerships. If partnership property has been debt-financed, as is often the case with real estate or alternative investment funds, then otherwise exempt rental income or investment income could be subject to UBTI. Additionally, if the organization finances its investment in the partnership, the income could be subject to UBTI.

Any unrelated trade or business income flowing through to an exempt organization from a pass-through entity can trigger UBTI. With investments in partnerships, the organization must look through to the underlying partnership activity and apply the UBTI rules as if the organization had conducted the activity directly. An exempt organization must include its proportional share of the partnership’s unrelated business activities when computing UBTI. However, allocable partnership income that otherwise would be excluded from the calculation of UBTI under Sec 512(b) is still excluded, such as investment income (that was not debt-financed).

Partnerships are instructed to use Schedule K-1, box 20, code V, to report UBTI information. Simply reporting the total gross income from UBTI activities does not satisfy the partnership‘s reporting obligation. The IRS indicates that an attachment should be provided showing the organization’s share of partnership gross income from the unrelated trade or business as well as its share of partnership deductions directly connected with the unrelated gross income. The IRS does not provide a format or discuss the information to be included on this attachment. Any statement should include the total gross UBTI as well as the deductions attributable to that income, so that the exempt organization can determine whether it has a filing requirement based on gross income before deductions. Partnerships will generally include a footnote on Schedule K-1 that reports the respective line items and the amount or percentage which is subject to UBTI.

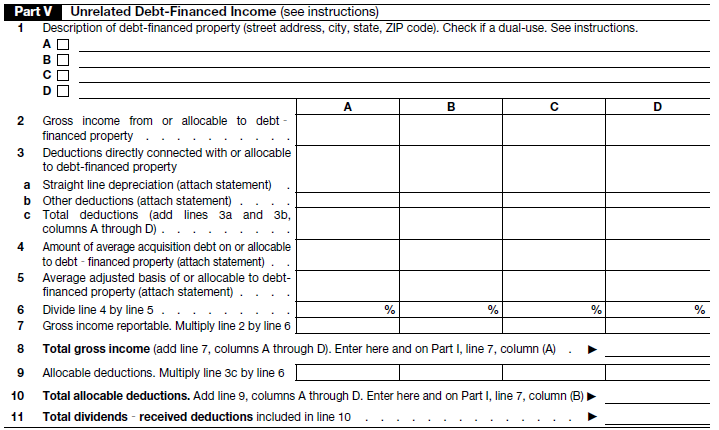

When reporting unrelated debit-financed income, only the percentage of the rental activity that is leveraged with debt is subject to UBTI. Schedule A of Form 990T includes part V for reporting and calculating debit financed property.

In Part V, the organization calculates the average acquisition debt on allocable debt by taking the beginning and ending debt balances and dividing by two. The organization also calculates the average adjusted basis by taking the beginning and ending historical cost of rental property less accumulated depreciation, and then divide by two.

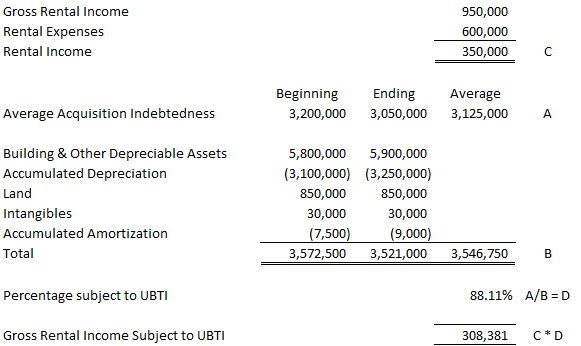

Below is an example of how unrelated debt-financed income is calculated.

Exempt organizations investing in partnerships should ensure that the K1 reporting from the partnership provides the information necessary to report UBTI under box 20, code V. An exempt organization may need to follow up with the partnership return tax preparer to obtain the information necessary for the exempt organization to report their UBTI on Form 990T. Reach out to a PBMares tax advisor if you have questions regarding UBTI reporting.

Be sure to consult with your financial or tax advisor on this topic as individual situations may vary. The information contained in this article or webinar, and any related materials, are for informational purposes only, and cannot be relied upon for legal, financial, tax, accounting, or other professional services advice. The content is provided on an “as is” basis and PBMares makes no representations or warranties about the accuracy or sustainability of any information for your purposes. For any specific questions you may have, please contact us.

This content is accurate at the time of publication. Always ensure you are reviewing the most recent information available. Contact your tax or financial advisor if you need clarification.

Contact Us

About the Author

Edward Yoder

CPA, MSA

Partner

Harrisonburg

Ed has a long-standing affinity for helping clients make sense of their debits and credits, showing how they fit together to tell the organization’s financial story.

View Bio