Posted by Charles Dean Smith, Jr. in Tax: Individual.

For many employers, November and the end of the year means open benefits enrollment. Health Savings Accounts (HSAs) have long been a popular tool to set aside money for healthcare expenses, but many people aren’t aware of the triple tax benefit. Even current HSA subscribers aren’t using these accounts to their full potential. The key to maximizing the benefits of an HSA is to understand how it can be used – and what the full range of tax benefits are.

HSAs are gaining popularity, partly due to the increase in high-deductible health plans (an HSA-eligible high-deductible health plan currently has a deductible of at least $1,350 for individuals and $2,700 for family coverage) and partly due to circumstance. Since 2011, the amount of HSA accounts has grown more than five times. Nationwide, there is about $93 billion held in HSAs versus $12 billion in 2011; that’s a 675 percent increase from ten years ago.

It’s estimated that one in three Americans don’t have one. Among those who do, 55% haven’t even contributed to it within a year[1].

The Triple Tax Benefit of HSAs

HSAs were created in 2003 when Medicare access expanded. They’re meant to help people with high-deductible health plans, and high out-of-pocket costs as a result, afford health care services. They are one of the most efficient tax-advantaged accounts currently available in that contributions are made pre-tax and any investment growth in the account is tax-free along with withdrawals if the money is used for qualified healthcare expenses.

Tax benefit number one: any money that’s set aside in an HSA isn’t subject to federal income tax.

Similar to a 401K or IRA, money put into an HSA goes in tax-free for federal income tax purposes. Most contributions are handled with pre-tax dollars through payroll deductions, so they are not included in taxable income when the income tax return is filed. Taxpayers can also choose to make contributions to their HSA account outside of payroll deductions. Self-employed taxpayers would report the HSA tax deduction directly on their individual tax return.

HSA accounts are very flexible compared to other tax-advantaged accounts such as IRAs.

Tax benefit number two: Withdrawals for qualified medical expenses are also tax-free.

There are at least 200 qualified healthcare expenses that money in an HSA can be used for. Over-the-counter medications, prescriptions, copays, hospital fees, common medical treatments, many surgeries, dental services, and much more all fall under common covered expenses. Some covered expenses may even be surprising: acupuncture, a doula, glasses, a guide dog, and overnight lodging related to a hospital stay are all covered expenses. Personal protective equipment used to prevent COVID-19, such as masks or hand sanitizer, are also now considered eligible expenses.

Plus, a 20 percent penalty for non-eligible withdrawals goes away after age 65 (but the amount would still be subject to the current regular income tax rates at the time of the withdrawal).

If financial situations permit, a great option for medical expenses is to use cash outside of the HSA account to pay for current medical expenses and electronically save medical receipts.

Then, use those saved medical receipts in later years to take tax-free distributions from the account to use for other large ineligible expenses such as tuition, travel, home repairs, or a down payment on a new home.

Most HSAs are flexible regarding the timeline for reimbursement of medical expenses as the medical expenses do not need to be incurred in the same tax year as a reimbursement from the account. So, get in the habit of electronically saving receipts for large eligible medical expenses in the event there could be a future HSA distribution for a large ineligible or unexpected expense.

Tax benefit number three: HSAs can be an investment vehicle with tax-free investment growth.

And finally, funds in an HSA can be invested in the stock market. This can be a great tactic to use when planning healthcare costs in retirement or over the long-term, as the money will generally grow faster than leaving it all in cash. Investors are more likely to stay ahead of inflation and have the money they need for future care, which can cost upwards of $300,000 for a couple who retires at age 65 in 2021.

There’s the very attractive option of letting account balances grow and using that money as part of an overall retirement strategy. This is a vastly underutilized benefit; around 90 percent of HSA subscribers only hold HSA benefits in cash; less than ten percent actually invest any part of their funds. Most HSAs offer investment options that are very similar to 401K investment offerings.

Unlike flex spending accounts (FSAs), HSAs are portable and can stay with the account holder through job changes. There’s no deadline to use the money, and funds aren’t subject to required minimum distributions in retirement unlike most other retirement accounts.

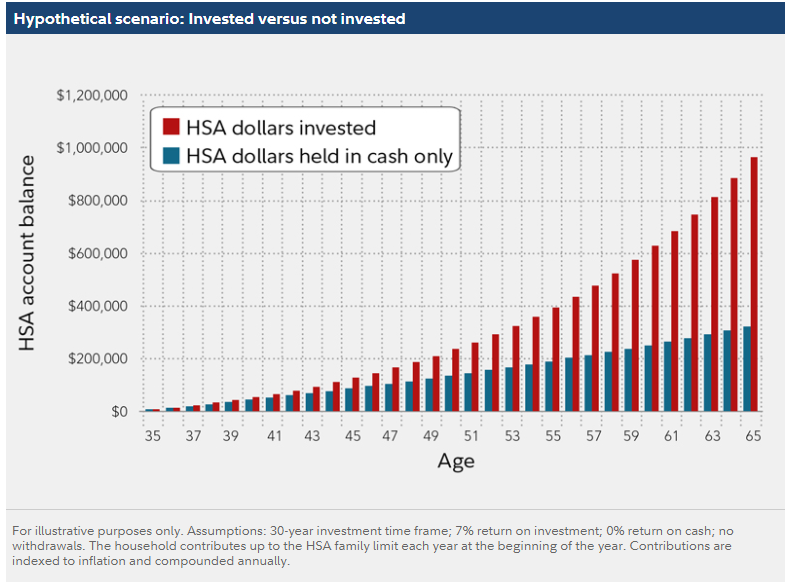

This chart from Fidelity clearly demonstrates the benefit of investing in an HSA versus holding the money in all cash. Over a 30-year period, the account balance can almost triple under certain circumstances.

In the article linked above, even an account holder who withdraws half their contributions for healthcare expenses still gets substantial benefits.

Strategies to Maximize an HSA

Americans with access to an HSA have a few strategies to make their money go further.

The best way to get the most out of an HSA is to contribute the annual maximum. In 2021, individuals can contribute $3,600 to an HSA, or $7,200 for family coverage. Account holders age 55 and older can make an extra $1,000 in contributions.

Some employers will match employee contributions, but the combination of employee-employer contributions can’t exceed the IRS’s limit. Independent contractors and self-employed individuals can open an HSA too and receive similar tax benefits from the contributions– if they have a high-deductible health plan.

Also, consider consolidating more than one HSA. This is a possible scenario if a taxpayer changed jobs and opened two different HSAs under two different high-deductible health plans. This would increase the account balance and open up the opportunity to invest.

Another option to reach that threshold is to transfer money held in an IRA or Roth IRA to an HSA. The money would grow tax-deferred and depositing a lump sum may allow more account holders to access a required minimum balance to invest.

Finally, invest! If the benefits plan allows it, it’s the best way to grow the account. Some plan administrators require a minimum HSA balance before the account holder can consider investing. Find out what this number is, and work towards it over time.

Treat the HSA like a supplemental 401K retirement account; consider it a means to accumulate long-term wealth. One way to do this is by keeping enough cash in the account to cover annual expenses and investing the rest. This can be helpful for anyone who might not be able to afford paying out-of-pocket (and without the HSA) to let funds accumulate.

How to Use an HSA in Retirement

Last but certainly not least, once taxpayers hit retirement there are other ways to use HSA funds besides for qualified medical expenses. We’ve already mentioned that the 20 percent penalty for non-qualified expenses goes away after age 65.

They can also help bridge the gap in insurance coverage if someone retires sooner than the age where Medicare kicks in; this is currently 65. HSAs can’t cover healthcare premiums except for COBRA subsidies through an employer-sponsored plan or when receiving unemployment compensation.

Then, once a taxpayer hits age 65, an HSA can be used to pay Medicare Part B premiums and Part D prescription coverage.

Long-term care policy premiums are also covered by HSAs – this is true regardless of age, but especially helpful in retirement.

Conclusion

HSA popularity will only grow in the future, and for many good reasons. Be aware that high income taxpayers may very well see their ability to contribute to Roth IRAs limited or even eliminated in certain tax proposals such as in the current Build Back Better tax legislation. This would make HSAs even more attractive in the future as a supplemental retirement fund with the only retirement account option likely remaining with a triple tax advantage.

The bottom line: if you’re eligible to contribute to an HSA, do it. Talk with your employer about eligibility, matching, and investment options. Charles Dean Smith, Jr., CPA and Partner in PBMares’ Tax practice, is also available to answer questions, especially for HSAs that will be used as part of a larger tax and retirement strategy.

[1] https://www.upi.com/Health_News/2020/07/17/Study-55-in-US-with-health-savings-accounts-dont-contribute-to-them/9401594992460/

Be sure to consult with your financial or tax advisor on this topic as individual situations may vary. The information contained in this article or webinar, and any related materials, are for informational purposes only, and cannot be relied upon for legal, financial, tax, accounting, or other professional services advice. The content is provided on an “as is” basis and PBMares makes no representations or warranties about the accuracy or sustainability of any information for your purposes. For any specific questions you may have, please contact us.

This content is accurate at the time of publication. Always ensure you are reviewing the most recent information available. Contact your tax or financial advisor if you need clarification.

Contact Us

About the Author

Charles Dean Smith, Jr.

CPA, MSA

Partner, Franchise Team Leader

New Bern

Charles focuses on providing manufacturing, distribution, restaurant and retail clients with tax compliance and consultation.

View Bio