Imagine you are one of the first 100 employees at an innovative technology company. You are passionate about the mission and enjoy working with your colleagues. You have also accumulated a significant amount of company stock during your tenure, but the share price is less than $5 and makes up a small portion of your portfolio. You are paying more attention to the work at hand.

From Multimillionaire to Bust in a Few Years

In less than a year, the stock is worth 10 times what you paid for it. Then the price doubles the following year. You hear stories of colleagues buying sports cars and going on lavish vacations. You have been with the company long enough to feel that the success is well warranted, but you wonder how long this ride is supposed to last. How do you handle a stock that has appreciated well over 3,000% and is now solely responsible for your newfound wealth?

And just as quickly as it grew, the stock price plummets back down from $100 to $10, effectively erasing nearly 90% of your net worth within a couple of years. Some of your colleagues are stuck paying off the large purchases that they made, and others may have to push off retirement indefinitely. Analysts on TV are calling it a bubble burst. Bloggers are saying they predicted this mess a long time ago. All you know is that you may never get your portfolio value back.

Difficulties of Managing Concentrated Stock

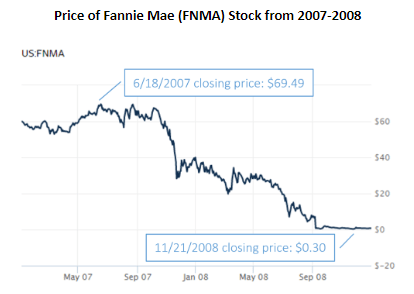

Employees of AOL, Fannie Mae, GE, and other companies throughout history have experienced these kinds of financial horror stories. Managing a concentrated stock position (often measured as over 10% of a portfolio) involves more than trying to predict the market. Selling a stock that has highly appreciated can incur substantial capital gains taxes. Holding concentrated stock can exacerbate portfolio volatility, and it is often an allocation oddball that can make proper diversification very difficult to achieve. High risk does not always equal high returns because idiosyncratic and company-specific risks may mean that the stock does not always rise with the overall market.

Source: The Wall Street Journal

Given the unique circumstances surrounding concentrated stock positions, there are some creative solutions that can reduce risk and alleviate the tax burden when implemented properly.

Hedging with Options

Owning an option means having the ability to buy or sell a stock at a specified price. Using an option strategy can be an effective way to limit a stock’s volatility and hedge downside losses.

How Hedging with Options works:

- Buy a protective put option, which gives you the right to sell your stock at a specific price. For a hypothetical stock trading at $100, buying a put at $95 limits your potential losses to $5 per share or 5% of the position’s value, even if the stock goes to $1.

- Sell a call option to create a “collar” because buying a protective put can be expensive. For a hypothetical stock trading at $100, selling a call at $105 gives the call owner the right to buy the stock from you at that price, even if the stock is worth more than that. You have effectively given up the upside of the stock to make downside protection more affordable.

What Hedging with Options means for concentrated stock:

If you are worried about your stock’s volatility but want to retain control of the position, setting up an options strategy can protect you from downside losses. However, some options strategies can trigger a sale that can incur tax consequences. Setting up a collar can also limit upside potential.

Charitable Remainder Trust

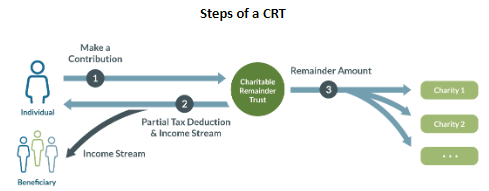

A charitable remainder trust (CRT) can receive a donation of assets and then generate a potential income stream for the donor or beneficiaries, with the remainder of the trust assets going to a designated charity or charities.

Source: Fidelity Charitable

How a Charitable Remainder Trust works:

- Contribute securities, real estate, private company stock, or cash to the trust and become eligible to take a partial tax deduction, which is based on the terms of the trust.

- Designate yourself or a beneficiary to receive a potential income stream for a term of no more than 20 years or the life of the beneficiary. The IRS states that the annual annuity payment must be at least 5% but no more than 50% of the trust’s assets.

- Once the trust terminates due to the time span or death of the last beneficiary, the remainder of the trust’s assets is distributed to the designated charitable beneficiary.

What a Charitable Remainder Trust means for concentrated stock:

If you contribute concentrated stock to a CRT, the trust can sell the position and reallocate the cash to a diversified portfolio, which reduces concentration risk. Assuming the stock is sold at a gain, you can also defer the payment of capital gains tax because the income beneficiary will pay tax on the income received from the trust over time. The trust itself can be an appropriate estate planning vehicle if your assets are subject to estate tax.

Exchange Funds

An investment in an exchange fund involves the tax-free swap of an acceptable stock for an interest in the fund, which can be diversified to match an index like the S&P 500. These are highly specialized, privately offered funds that are only available to investors that meet certain qualifications.

How Exchange Funds work:

- Determine if an exchange fund will accept shares of your specific stock, and evaluate the terms of the fund for minimum contributions, fees and commissions, and redemption restrictions.

- Swap shares of your stock for a pro-rata share of the exchange fund and manage the diversified position in relation to your overall portfolio.

After a set period of typically seven years, your interest in the fund can be redeemed.

What Exchange Funds mean for concentrated stock:

By swapping concentrated stock for an exchange fund that is diversified, you can reduce concentration risk without incurring a tax consequence from a sale. You defer any tax consequences until you redeem and decide to sell your share of the exchange fund.

Which Strategy Is Right for Me?

Investors can accumulate concentrated stock in multiple ways, whether through executive compensation, gifts, or legacy positions. Even though concentration risk can be highly detrimental to your portfolio, tax consequences and emotional ties to a stock can make it difficult to diversify. Putting in place a plan that is customized to your unique stock concentration issues can help achieve your financial goals.

Questions? Contact PBMares’ Wealth Management team today.

*This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting, or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness, or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Third-party economic or market estimates discussed herein may or may not be realized and no opinion or representation is being given regarding such estimates. Products and services herein may not be available in all jurisdictions or to all client types. The use of tools cannot guarantee performance. Diversification does not guarantee a profit or protect against loss in declining markets. As with any investment, there is the possibility of profit as well as the risk of loss. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

About the Author:

Daniel H. Yoo, CFP®, CEPA®, CM&AA®

Daniel H. Yoo, CFP®, CEPA®, CM&AA®

Senior Wealth Advisor

As a Senior Wealth Advisor and Certified Financial Planner™, Daniel Yoo simplifies the financial lives of entrepreneurs, executives, and their families. He is also a Certified Exit Planning Advisor® to help business owners understand and optimize the value of an exit strategy.