Posted by Jennifer French in Construction.

The construction industry has been up and down the past few months. What seemed like a rebound in August going into September turned around by December. Early in 2021, backlogs are down, prices are up, and contractor optimism remains.

Looking Back

When COVID-19 first hit the U.S. earlier in 2020, construction’s place as an essential industry helped to bolster initial fears of a sector-wide downtown. Not all states recognized construction as essential, and even in those that did, contractors faced myriad issues getting employees back to work. The new economic and business environment was highlighted by worker shortages, supply chain disruptions, price increases, new safety mandates, and more.

As a result, an industry that already operated on thin profit margins has been stretched even further. Yet, as 2020 progressed, cautious optimism remained.

Current Conditions

The present outlook for construction is mixed. Interest rates at all-time lows mean that contractors can maintain higher levels of debt, and certain tax-advantaged strategies like bonus depreciation and NOL carrybacks can help to leverage large purchases or losses in the current or previous year(s). But underwriting is more difficult in a tougher lending environment.

Construction is still essential and most likely won’t be totally shut down by government mandates again, but projects are stalled or canceled altogether. Projects that were already underway were safe; now, the effect of COVID-19 on many industries means that less money is available to finance and fund new projects.

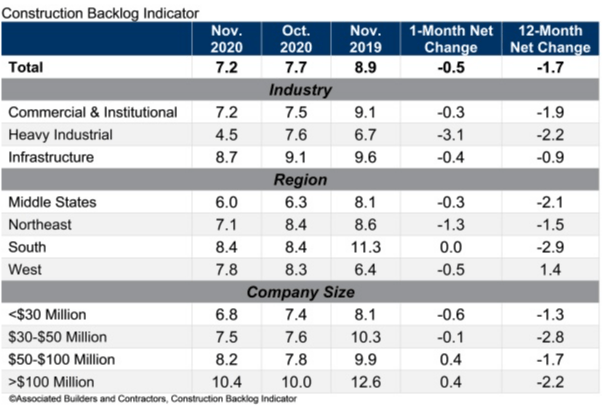

Evidence of this is in the latest Construction Contractor Index, which sees backlogs down by 0.5 month from the previous period, and down overall -1.7 months from a year ago. Heavy industrial continues to fare better in the current term but is down the most from a year ago.

Source: Associated Builders and Contractors

ABC’s current leading indicators for the construction confidence index are listed below. Comparisons are to the previous month.

- Sales expectations: 49.4 (down 6.26%)

- Profit margin expectations: 43.4 (down 7.86%)

- Staffing level expectations: 53.8 (down 4.95%)

It is promising that many contractors expect their staffing needs to stay the same or expand slightly over the next six months. While profit and sales expectations are lower, it doesn’t appear as if the industry is bracing for another recession.

What’s Ahead for Construction in 2021

At the time of this writing, at least two COVID-19 vaccines have begun U.S. distribution. This is promising and a reminder that the end is in sight – even if it may still be months into the future. Construction has regained 63.6 percent of its pre-pandemic jobs, representing the third best performing sector according to a recent report in Construction Executive.

Earlier in the fall, ABC Chief Economist Anirban Basu cautioned that uncertainty remains in the coming months. Some markets, like luxury real estate and e-commerce, have done quite well in the pandemic. Others, like retail, hospitality, and Class A office space, are still figuring out a new way forward. Positives for the industry include additional federal stimulus dollars thanks to a new relief bill at the end of 2020, and certain expenses paid with PPP forgivable funds are officially tax deductible. Plus, Congress formally recognized that forgiven PPP loans will be treated as non-taxable income.

Government investments in transportation, water and sewage, and telecommunications projects should continue to drive infrastructure construction forward. Commercial and institutional construction may be able to expand upon project opportunities for renovations and retrofits now that COVID-19 health guidance is expected to change how buildings are designed and laid out. And Class B office space could be another opportunity to develop and/or renovate as it presents tenants with more flexibility and better pricing than its Class A counterparts.

Strategies to Mitigate Ongoing Risk

Given that profitability and industry optimism will continue to be volatile over the next several months, contractors can proactively manage their business through:

- Expanding relationships with different suppliers and vendors

- Pre-buying higher-in-demand materials to lock in lower prices

- Training staff on core skills, investing in staff development, and diversifying industry verticals

- Bidding only on work for which the contractor is uniquely qualified to do, and being extremely careful in the bidding process not to lower pricing

- Revisiting the contract and ensuring appropriate language is in place to cover unexpected delays or price increases

- Conducting cash flow and profitability analyses

- Performing advance tax planning to take advantage of CARES Act and other year-end tax incentives

For now, contractors will need to stay the course, adjust as needed, and continue to plan for an uncertain future. The results of Georgia’s runoff Senate elections mean that the Senate will hold a slim Democratic majority, meaning the likelihood for tax changes could be higher in 2021 or 2022. For more guidance on construction business management, growth, and tax strategies in a volatile market, reach out to your PBMares advisor or Jennifer French, CPA, Partner, and Team Leader of the Construction and Real Estate group.

Questions? Contact your PBMares Tax Advisor today!

Be sure to consult with your financial or tax advisor on this topic as individual situations may vary. The information contained in this article or webinar, and any related materials, are for informational purposes only, and cannot be relied upon for legal, financial, tax, accounting, or other professional services advice. The content is provided on an “as is” basis and PBMares makes no representations or warranties about the accuracy or sustainability of any information for your purposes. For any specific questions you may have, please contact us.

This content is accurate at the time of publication. Always ensure you are reviewing the most recent information available. Contact your tax or financial advisor if you need clarification.

Contact Us

About the Author

Jennifer French

CPA

Partner, Construction Team Leader

Newport News

Jennifer specializes in tax planning and structuring of complex transactions for partnerships, limited liability companies and individuals in construction and real estate, including construction contractors, land developers and real estate and rental property owners.

View Bio