Source: RSM US LLP.

REAL ECONOMY BLOG | January 11, 2024

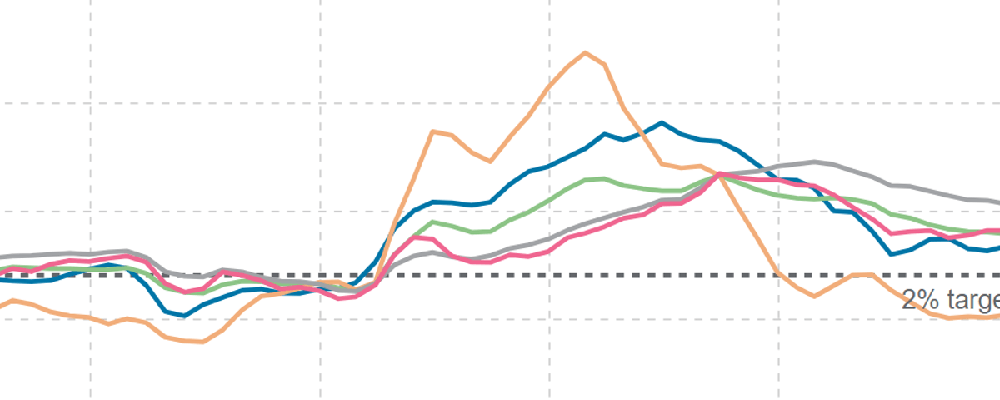

The December Consumer Price Index captures both the broader disinflation taking place inside the goods sector and the persistent inflation inside the service sector.

Prices in the service sector, which comprises 62% of the overall index, increased by 5% on a year-ago basis.

Each generates its own economic and policy narratives that carry implications for the economy in a year of a closely fought election.

Despite a three-month annualized top-line inflation pace of 1.8% and a six-month rate of 3.3%, prices in the service sector, which comprises 62% of the overall index, increased by 5% on a year-ago basis, according to government data released on Thursday.

This stickiness in the pricing of services strongly suggests that the Federal Reserve will show caution as it lays the groundwork for rate cuts.

But sustained easing in inflation amid a strong labor market has resulted in real wage growth, which increased by 0.8% from a year ago.

From our vantage point, that increase is the major economic narrative as we embark on what will be a contentious election year in which we expect the CPI to fall to 2.5% or lower.

On a year-ago basis, the top-line CPI increased by 3.4% through December while service sector inflation advanced at a much more challenging 5%. That dynamic is a good example of why expectations around a March cut in the federal funds rate are premature.

In December, top-line inflation and the core metric, which excludes food and gasoline, both advanced by 0.3% and were up by 3.9% from a year ago. The major catalyst for the overall increase in inflation was the 0.4% rise in housing, which comprised roughly half of the increase in the overall index. Housing costs increased by 4.8% from a year ago.

Policy implications

Persistent inflation inside the service sector, along with December’s core and super-core measures of inflation, all point toward the Fed holding rates steady at its January meeting and to the repricing of expectations around a March rate cut.

We have never been in the camp that expects a cut in March. Our forecast of four 25 basis-point rate cuts this year, starting in June, stands in contrast with the current consensus of rate cuts this year. The December inflation data, risks to the outlook and the likely evolution of pricing do not point to a rapid pivot by the Federal Reserve.

While inflation will continue to ease, we have made the case that the endgame in the Fed’s efforts will not necessarily result in a 2% rate over the long term. The evolution of the data illustrates just how difficult the last mile will be.

The data

Energy prices, which have been the major driver of disinflation over the past few months, increased by 0.4% in December while transportation costs increased by 0.2%, new vehicles by 0.3% and airline fares by 1%.

Shelter costs and the policy-sensitive owner’s equivalent rent series increased by 0.5%. Food at home increased 0.1% and the price of food and beverages grew by 0.2%.

Medical care costs jumped by 0.6% and recreation by 0.4% while education and communications costs increased by 0.1%

The takeaway

The last mile of the inflation fight will not follow a straight line back to the Federal Reserve’s 2% target. Rather, persistent inflation inside the service sector and stubborn housing costs will pose obstacles. We think top-line inflation will end the year at or below 2.5%.

But the overall slowing of inflation is resulting in rising real wages above inflation, which were up by 0.8% on a year-ago basis. That increase will put a floor under the slowing in overall economic activity that we expect in the near term.

This article was written by Joseph Brusuelas and originally appeared on 2024-01-11. Reprinted with permission from RSM US LLP.

© 2024 RSM US LLP. All rights reserved. https://realeconomy.rsmus.com/december-cpi-sticky-service-and-housing-prices-illustrate-the-difficult-last-mile-in-inflation-fight/

RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent assurance, tax and consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmus.com/about for more information regarding RSM US LLP and RSM International.